While Circle exceeded revenue expectations, its profits still heavily rely on its reserves. The amount of USDC in circulation has held steady despite fluctuations in crypto prices. However, new regulations concerning how reserve income is shared could create problems for its important partnership with Coinbase.

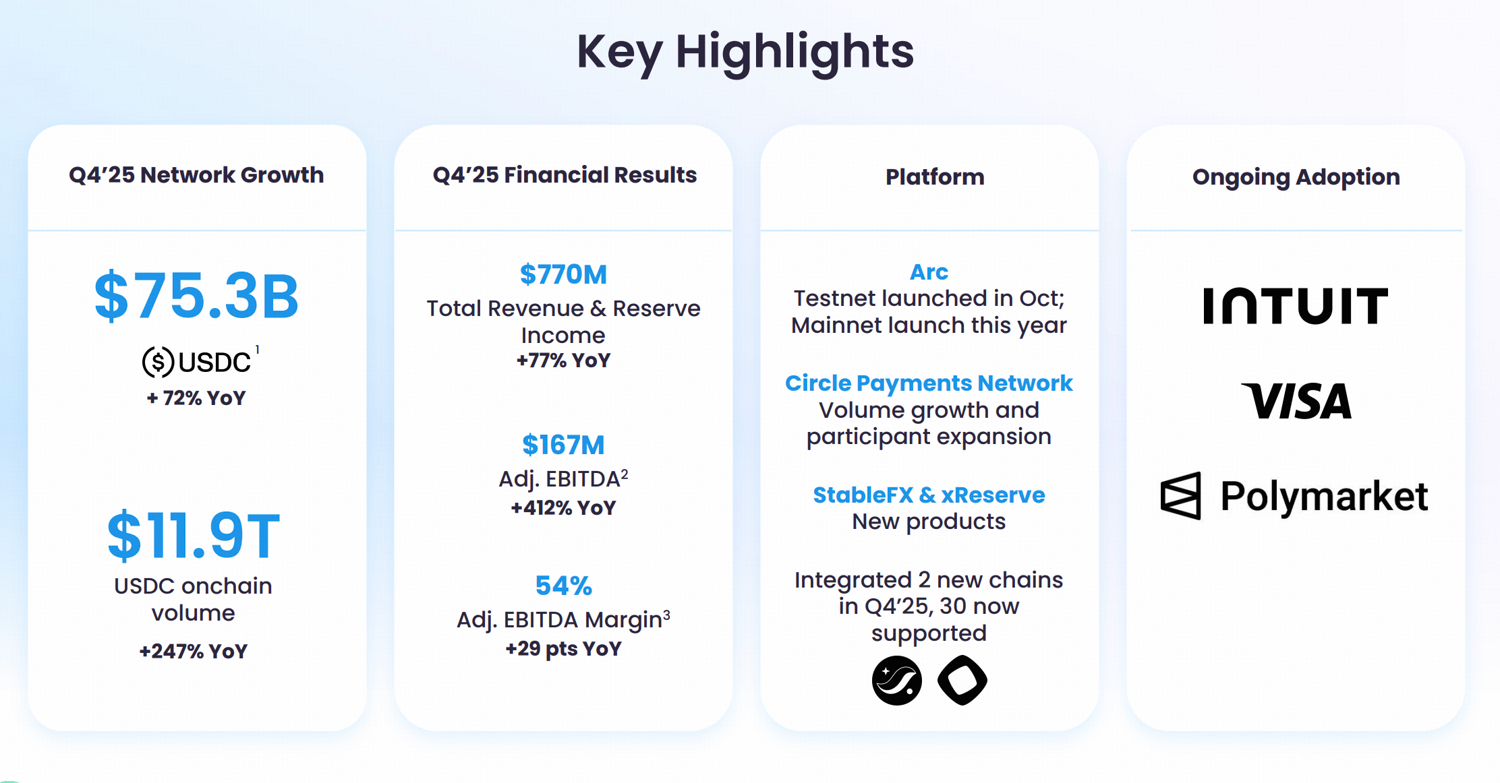

Circle announced strong financial results for the last quarter of 2025, earning $770 million in revenue and reserve income. They also reported a significant increase in the amount of USDC in circulation, reaching $75.3 billion – a 72% jump compared to the previous year. Investors reacted positively to the news, and the company’s stock price immediately increased.

The deeper investment takeaway sits beneath the headline revenue beat.

- Circle’s earnings model can be framed as “rate + USDC scale + distribution economics”, though the company is trying to reposition itself toward payment infrastructure and application-layer revenue streams.

- Despite an almost 50% decline in Bitcoin’s price and the broader crypto market weakness, total stablecoin supply remained stable, a dynamic not seen in prior crypto bear market. Stablecoins have decoupled from crypto market price volatility, making the “scale” component in Circle’s business model less of a concern.

- The real uncertainty now lies in distribution economics. Recent OCC interpretations tied to the GENIUS Act raise questions about whether exchange-based reward structures linked to USDC could be viewed as impermissible yield pass-through. If regulators constrain how reserve income can be shared through distribution partners, the long-standing Circle–Coinbase commercial arrangement may face pressure.

Brief Q4 Snapshot & Circle’s Earning Model

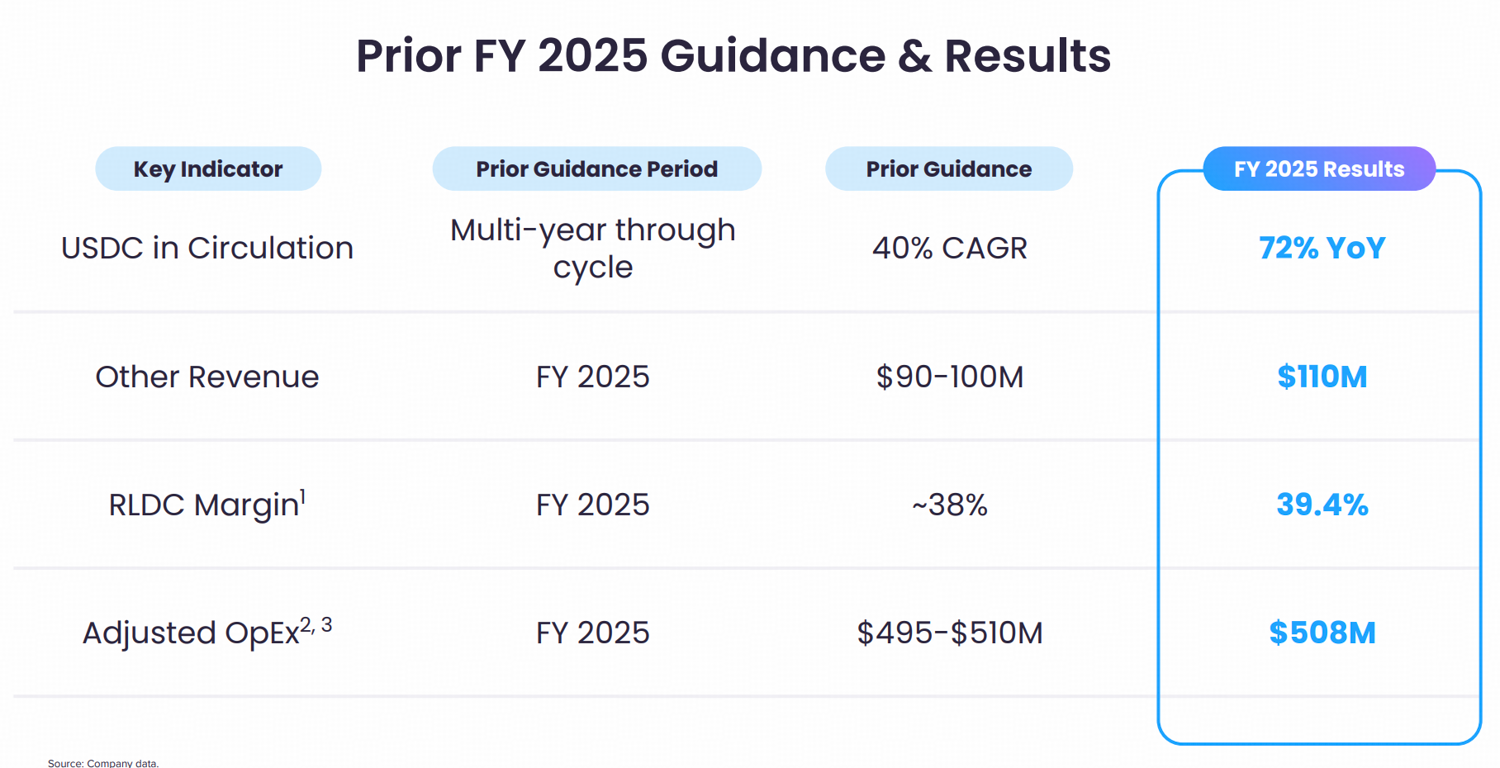

As I reviewed Circle’s latest earnings report for Q4 2025, I noted they ended the year with $75.3 billion of USDC in circulation. Total revenue and income from reserves reached $770 million. Importantly, management reaffirmed their expectation of a 40% compound annual growth rate for USDC in circulation over the long term, even accounting for market cycles.

Two details about Circle’s business model stand out:

Currently, most of Circle’s revenue comes from the income earned on its reserves. In the last quarter, they reported $733 million in reserve income, a 69% increase compared to the same time last year. However, the rate of return on these reserves decreased slightly to 3.8%, down from the previous year. Despite lower interest rates, the increasing amount of USDC in circulation has resulted in overall revenue growth.

Also, Circle spent $461 million on things like distributing USDC and processing transactions in the fourth quarter, which is a 52% increase. This shows they still depend a lot on partnerships, especially their deal with Coinbase, to get USDC widely used.

Circle makes money through a combination of interest rates, the widespread use of its USDC currency, and how it shares revenue with its partners. Specifically, interest rates impact how much profit Circle earns on its reserves, the popularity of USDC expands the size of those reserves, and agreements with partners define how revenue is split.

The company is growing by adding payment systems and blockchain technology to its offerings, which will lessen its dependence on income from reserves and exchange activities. In 2025, revenue from these new sources – excluding reserves – totaled $110 million, exceeding expectations.

Our main offerings include Circle’s payment network, which allows for fast, global money transfers using stablecoins and operates with licenses in 55 countries and regions (including U.S. money transmitter licenses and compliance with European regulations); Arc, a blockchain platform designed for businesses to build financial applications; and tools for developers, like the Cross-Chain Transfer Protocol, to easily move funds between different blockchains.

Although Circle still primarily earns revenue from reserves, the increasing income from infrastructure services suggests a positive shift in the company’s business model.

Stablecoin Decoupled from Crypto Market Price Fluctuation

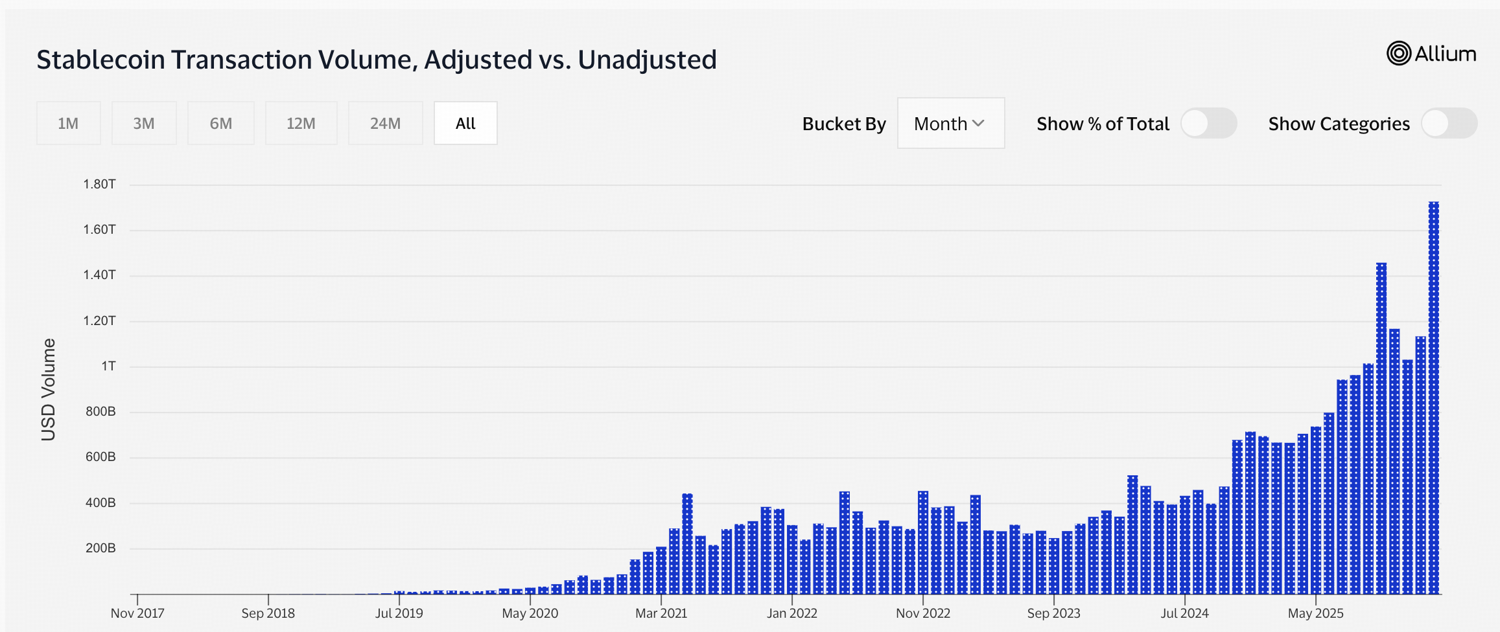

Even though Bitcoin’s value has dropped nearly 50% from its high point in late 2025, the total supply of stablecoins has stayed fairly consistent, not decreasing much during the recent market downturn. According to Defillama, the total value of stablecoins is around $310 billion, which remains very high compared to historical levels.

Despite a significant downturn in the cryptocurrency market – with indicators showing extreme fear – stablecoin transaction volume reached a record high of $1.73 trillion in February 2026, according to Visa data.

This situation is unlike previous downturns. In the past, similar drops in value usually led to issues with stablecoins – like them losing their set value or large amounts being withdrawn – and a general loss of money from the crypto market. This time, those things aren’t happening.

Several structural factors may explain this divergence.

By 2026, stablecoins are expected to be much more than just tools for buying and selling cryptocurrency. They’ll be commonly used for international payments, payments directly on blockchains, and even helping companies manage their finances. This wider range of uses means the total amount of stablecoins in circulation won’t be as closely tied to risky crypto trading.

The systems supporting the market have also become more developed. With clearer information about reserves, better monitoring of those issuing assets, and closer connections to established financial systems, the risk of chaotic sell-offs during periods of market fluctuation has decreased.

Circle’s business thrives when its stablecoins remain reliable and widely used, as this strengthens the foundation of its reserves, which generate income. Because the number of stablecoins in circulation is now less affected by the ups and downs of the crypto market, Circle’s profits are also becoming more stable. However, Circle’s stock price still tends to move dramatically with the crypto market, behaving more like a risky investment than a reflection of the company’s improving core business. As more people and businesses use stablecoins, this disconnect could lessen, potentially leading to a more accurate valuation of Circle’s stock.

Distribution Economics and Regulatory Risk

The biggest challenge for Circle is how regulations will affect its ability to share profits, which impacts its overall business model.

A new conflict is developing regarding how profits earned from the reserves backing stablecoins can be shared. The U.S. Office of the Comptroller of the Currency has indicated it will likely interpret a law called the GENIUS Act to prevent stablecoins from paying interest. If this interpretation is made final, it could impact programs that use reserve income to reward users, directly affecting how Circle and Coinbase currently work together.

The GENIUS Act prevents companies that create stablecoins from offering interest on them. Previously, most in the industry believed this rule only applied to companies directly offering returns. However, a new proposal from the Office of the Comptroller of the Currency (OCC) is questioning that understanding.

The report suggests that close financial relationships between companies issuing crypto tokens and the platforms that manage them strongly indicate that rewards are being passed on to token holders through a third party. Specifically, if a token issuer shares profits with a partner who then offers rewards based on stablecoin holdings, regulators may see this as an illegal way of providing yield. Currently, Circle shares a large portion of its reserve income with Coinbase as part of their agreement. This encourages Coinbase to promote USDC and reward users for holding it, which is important to Circle because Coinbase’s broad customer base helps increase USDC usage.

The new rules from the OCC might cause regulators to examine reward programs offered through exchanges. If these programs are seen as directly tied to the income banks set aside as reserves, the way rewards are currently distributed could be questioned.

For investors, this affects how well Circle generates revenue from USDC, specifically how efficiently it’s promoted through cryptocurrency exchanges. While Circle is exploring other ways to distribute USDC, exchanges are currently the primary method.

Bottom Line

Interest rates naturally go up and down, but USDC has proven to be surprisingly stable during the recent downturn in the crypto market. Now, the biggest question is how these digital currencies will be distributed and used going forward.

Until the Office of the Comptroller of the Currency finishes its new rules and it’s clear how rewards from other companies will be handled, the way Circle and Coinbase share revenue currently poses the biggest threat to Circle’s near-term profits.

Read More

- Gold Rate Forecast

- Looks Like SEGA Is Reheating PS5, PS4 Fan Favourite Sonic Frontiers in Definitive Edition

- Pluribus Star Rhea Seehorn Weighs In On That First Kiss

- Arknights: Endfield – Everything You Need to Know Before You Jump In

- Dune 3 Gets the Huge Update Fans Have Been Waiting For

- 10 Steamiest Erotic Thriller Movies of the 21st Century

- Antiferromagnetic Oscillators: Unlocking Stable Spin Dynamics

- 22 actors who were almost James Bond – and why they missed out on playing 007

- 5 Weakest Akatsuki Members in Naruto, Ranked

- Action Comics #1096 is Fun Jumping-On Point for Superman Fans (Review)

2026-03-06 16:34