As a researcher studying economic trends, I can tell you that our current era is marked by an unprecedented capacity for modernization and digitization in all aspects, including the financial sector. A few years ago, physical currency in the form of gold and banknotes held sway; however, we are now on the brink of cash being superseded by digital money.

In order to facilitate the seamless transfer of digital funds, it is essential to have various mechanisms at our disposal. Among these are payment gateways and virtual terminals. Although these terms are frequently used synonymously, they actually refer to distinct components of the digital payment infrastructure. Let’s delve into their differences.

Key Takeaways:

- A payment gateway is a customer-facing platform for online transactions, while virtual terminals empower merchants with manual entry capabilities.

- Implementing the proper payment processing solution enhances efficiency, security, and client satisfaction.

- Use payment gateway and virtual terminal to streamline transactions and drive business growth in the digital landscape.

What Is a Payment Gateway?

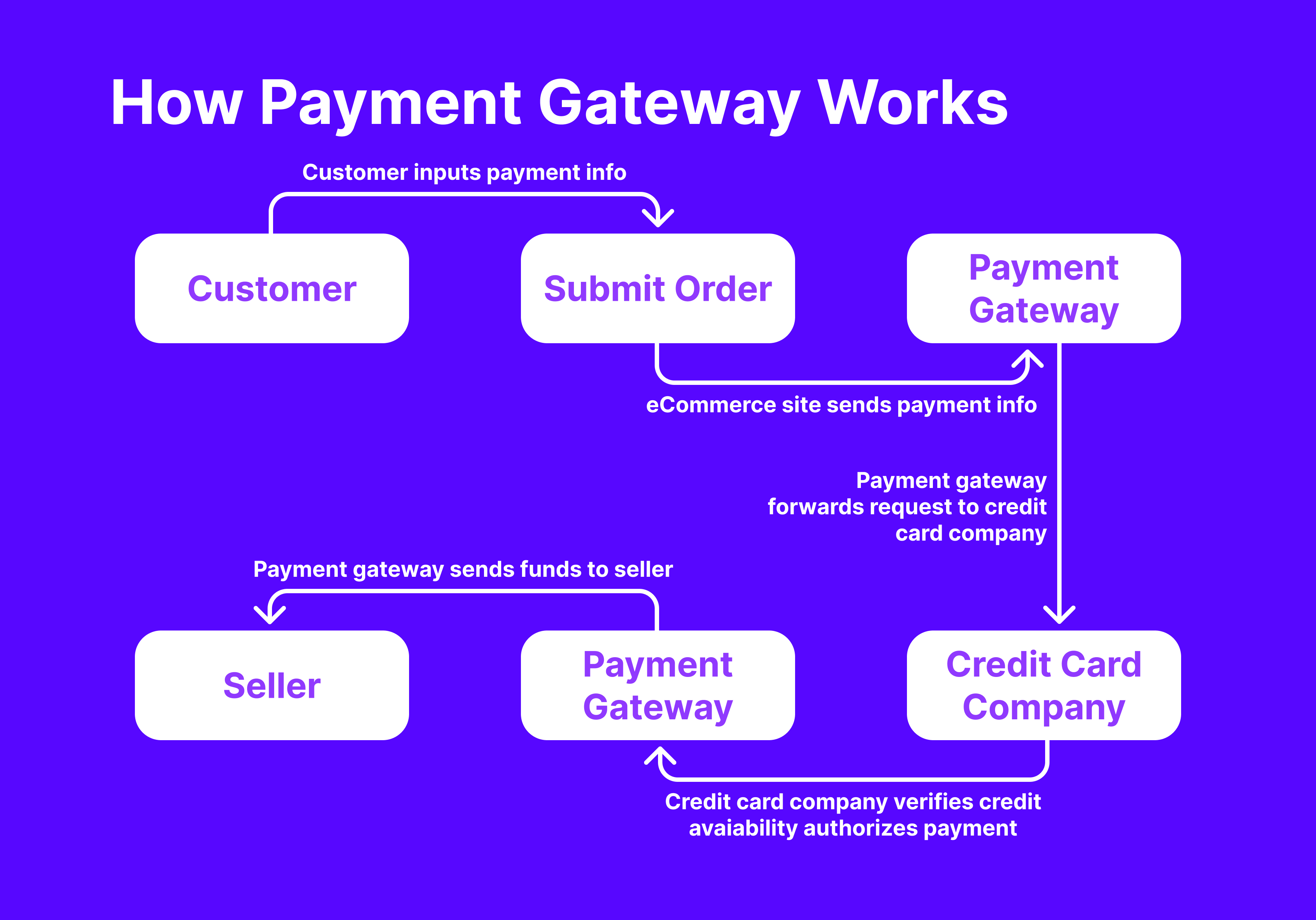

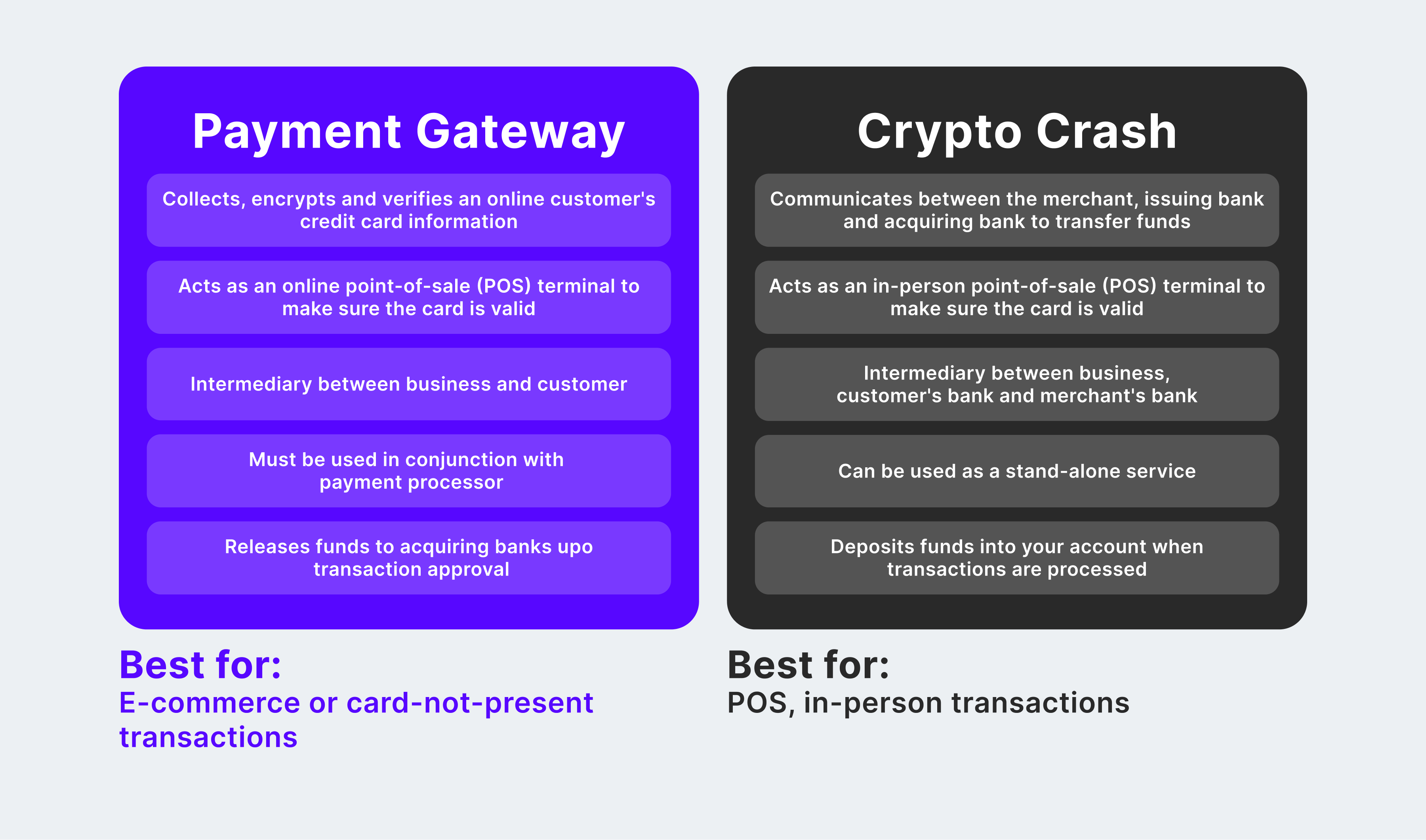

A payment gateway is a user-friendly digital solution that facilitates smooth online transactions. It serves as a bridge connecting merchants and customers, ensuring secure processing and confirmation of payments for bought products or services over the internet.

The gateway functions as a digital equivalent of a physical checkout desk, enabling customers to enter their payment information on a website or via merchant-supplied links. Once submitted, the system converts this confidential data into secure tokens before transmitting it to the payment processor, ensuring protection throughout the entire transaction.

Key Characteristics

A payment gateway functions as a bridge between a business’s website or application and the banking institution responsible for processing transactions. It allows customers to securely input their payment information, such as credit card numbers or bank account details, while completing a purchase.

After receiving the necessary data from the gateway, the payment processor checks it against the customer’s banking information for verification. Once approval is granted, the payment gateway sends a confirmation message to the merchant, enabling them to proceed with processing the order.

A payment gateway simplifies the transaction experience for businesses and consumers when buying or selling products and services digitally. It accepts multiple payment types such as credit/debit cards, electronic wallets, bank transfers, and alternatives like PayPal or Apple Pay.

As a researcher studying payment processing systems, I have discovered that providing various payment methods through a gateway broadens the scope of customers who can finalize their transactions.

Security Features and Encryption Protocols

Protecting sensitive financial information and preventing fraud is of the utmost importance for payment gateways. To accomplish this, they utilize encryption methods like SSL (Secure Socket Layer) or TLS (Transport Layer Security). These techniques scramble data during transmission from the customer’s device to the gateway, ensuring secure communication.

They frequently employ tokenization in addition to this, which involves substituting sensitive credit card details with distinctive codes (tokens), thereby safeguarding cardholder information from unauthorized usage. Furthermore, the payment processor observes PCI DSS regulations, ensuring a secure platform for handling transaction data.

Fast Fact:

A payment gateway serves as a bridge for transferring consumers’ payment details to merchants during transactions. In traditional retail outlets, this function is fulfilled by POS systems, which capture credit card info via terminals at checkout counters or contactless phones.

What Is a Virtual Terminal?

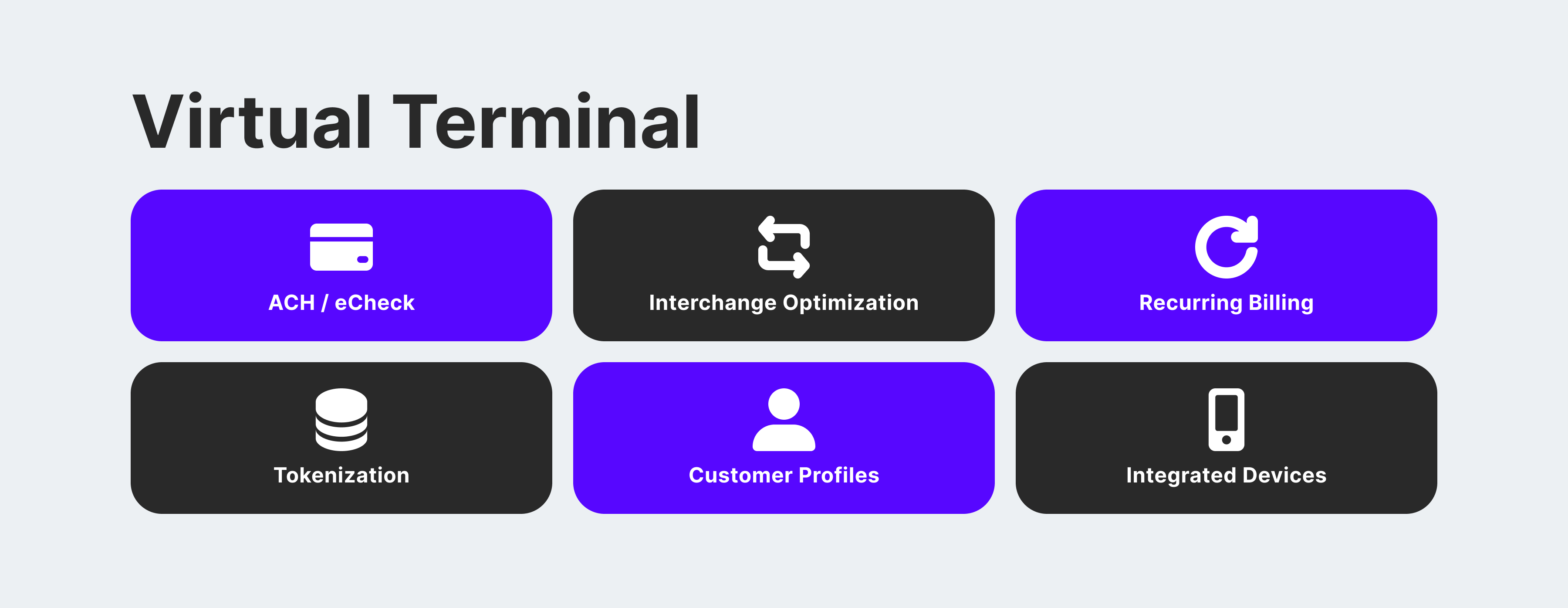

Online interfaces offered by payment gateways and merchant services allow businesses to input and process credit card transactions manually through virtual terminals.

In contrast to conventional cash registers, virtual terminals found online can be accessed via a web browser. This feature enables merchants to process transactions without the necessity of owning specific hardware. The primary function of these virtual terminals is to enable card-not-present sales, where the cardholder and merchant are not in the same location during the transaction.

As an analyst, I would explain that a virtual terminal represents a user-friendly interface specifically designed for merchants within their account for virtual terminal transactions. This tool serves as a control panel, enabling merchant service providers to process credit card information for sales conducted offline, such as over the phone, via email, or through digital invoices. Different from payment gateways that cater to customers, a virtual terminal grants merchants backstage access to effectively manage their transactions.

Key Features

Businesses can access virtual terminals from any device connected to the internet, enabling them to take payments on-the-go. These interfaces are designed with simplicity in mind, allowing merchants to easily input payment details and complete transactions promptly.

Virtual terminals can handle several currencies, enabling businesses to receive global payments from customers. These platforms typically offer functionalities for overseeing transactions, including checking past transactions, producing reports, and processing refunds.

Virtual terminals provide the capability to establish regular payments through their features, making them ideal solutions for businesses that operate on a subscription model.

Security Considerations and Compliance

Virtual terminals employ security measures like SSL/TLS encryption to safeguard the transfer of confidential payment information online, preventing unauthorized entities from accessing it during transmission.

Businesses that utilize virtual terminals are obligated to comply with the Payment Card Industry Data Security Standard (PCI DSS) to maintain the secure processing and retention of cardholder data. A common practice among these virtual terminals is implementing tokenization, which substitutes sensitive card details with distinct identifiers (tokens), thereby decreasing the risk linked to saving payment information.

Virtual terminals come equipped with integrated security features for minimizing fraud. These features encompass measures like address confirmation and velocity screening, which help safeguard against potentially unauthorized transactions.

As a business analyst, I’d summarize it this way: Virtual terminals enable me to process card-not-present transactions in a hassle-free and secure manner. They come with essential features like accessibility, user-friendliness, the ability to support multiple currencies, and robust security protocols.

As a security analyst, I would recommend that businesses adhere to security guidelines like PCI DSS to ensure the protection of sensitive customer information. Additionally, implementing encryption and tokenization techniques is crucial for safeguarding data during transmission and storage. By doing so, businesses can effectively reduce the likelihood of data breaches and fraudulent activities while maintaining a smooth payment process for their valued customers.

Realising the Distinctions: Payment Gateway vs Virtual Terminal

As an analyst, I would explain that the main difference between a payment gateway and a virtual terminal is in their target audiences and capabilities. A payment gateway serves the end-users by enabling them to make online purchases, whereas a virtual terminal enables merchants personally to process transactions manually when dealing with offline or non-internet sales.

Let’s compare the virtual terminal and payment gateway across the specified aspects:

Cost Implications

The initial expenses for virtual terminals tend to be lower with little to no upfront costs and typically no monthly charges. However, integrating a payment gateway may involve higher setup fees, which can range from a few hundred to several thousand dollars based on the chosen provider and desired level of customization.

The cost for processing transactions using virtual terminals tends to be higher than that of payment gateways. Fees for virtual terminal transactions typically amount to between 2.5% and 3.5% per transaction, along with a set charge. In contrast, fees for payment gateway transactions usually begin at around 1.5% to 2.9% per transaction, accompanied by a fixed fee.

Flexibility

For businesses handling fewer transactions, functioning in service sectors, or predominantly conducting operations online or offsite, virtual terminals are an ideal choice. Equipped with fundamental capabilities such as invoicing, regular billing, and client management, these terminals can be easily tailored to diverse business structures.

For companies handling larger numbers of transactions or operating online stores, as well as those seeking sophisticated functionalities such as inventory control and shopping cart integration, a payment gateway provides an ideal solution. Rich in features and adaptable to various industry requirements, it offers a multitude of customization options.

User Experience

As a crypto investor, I find virtual terminals to be incredibly convenient with their uncomplicated and streamlined interfaces. Setting them up is a breeze, and navigating through the features is as natural as breathing. While customization options might not be as extensive as those offered by payment gateways, I can still personalize my experience with primary branding and configuration adjustments.

Payment gateways offer more complex user interfaces, rich with customization features and compatibility with various e-commerce sites. The setup procedure can be intricate, particularly for businesses linking to existing systems. However, this added complexity brings greater adaptability and expansion capabilities over time.

Use Cases and Suitability: Virtual Terminal vs Payment Gateway

As a crypto investor, I’ve come across various payment solutions like virtual terminals and payment gateways. For smaller businesses or investors with simpler transaction needs, using a virtual terminal is a cost-effective and user-friendly choice. However, for larger businesses or investors dealing with higher volumes and complex requirements, opting for a payment gateway provides more flexibility, scalability, and enhanced security features.

Let’s explore the benefits of payment gateways for e-businesses, virtual terminals for service-focused enterprises, and key factors for organizations handling transactions in both digital and physical realms.

E-commerce Businesses (Payment Gateway)

- Payment gateways offer a seamless checkout experience for e-commerce businesses, allowing customers to securely pay for goods and services online using various payment methods.

- The payment gateway integrates smoothly with popular e-commerce platforms like Shopify, WooCommerce, Magento, etc., enabling businesses to manage their online storefronts and payment processing in one centralized location.

- International payment gateways support multiple currencies and international transactions, facilitating sales to customers worldwide and expanding the reach of e-commerce businesses.

Service-Based Businesses (Virtual Terminal)

- Virtual terminals enable service-based businesses, such as consultants, freelancers, and professional services, to accept payments from clients without the need for physical card terminals.

- Service-based businesses can access virtual terminals from any location with an internet connection, allowing them to accept virtual terminal payments while on the go or working remotely.

- Virtual terminals often include invoicing features, allowing service-based businesses to generate and send invoices to clients easily, track payments, and manage billing cycles.

- Virtual terminals typically have lower setup costs and transaction fees than traditional payment terminals, making them a cost-effective solution for service-oriented businesses with lower transaction volumes.

Hybrid Models (Considerations for Businesses with Both Online and Offline Transactions)

- Businesses with online and offline transactions should consider payment solutions offering seamless integration between virtual terminals and payment gateways. This allows them to manage all payment channels from a single platform.

- Look for a payment service provider that offers omnichannel capabilities, enabling businesses to accept payments across multiple channels, including in-store, online, mobile, and over the phone, while maintaining a consistent and integrated customer experience.

- For businesses selling physical products both online and offline, integration between payment systems and inventory management software is essential to ensure accurate stock levels and streamline order fulfillment processes.

- Businesses should prioritize payment solutions that provide robust customer data management capabilities, allowing them to track customer interactions and purchase history across all channels to understand better and engage with their customer base.

Challenges and Limitations

Let’s explore the challenges and limitations associated with payment gateway and virtual terminal:

Technical Issues and Downtime

As a crypto investor, I’ve experienced firsthand the frustration of encountering technical issues with payment gateways that disrupt my transactions and potentially result in lost opportunities for profit. During high transaction volumes or surges in traffic, such as during holidays or sales events, these systems can become overwhelmed, leading to delays or even interruptions in service. These disruptions not only affect me as an individual investor but also pose significant challenges for businesses that rely heavily on seamless payment processing to drive revenue growth.

A virtual terminal functions by relying on a stable internet connection, meaning any interruptions to your internet service or problems with the hosting servers could disrupt transaction processing. Furthermore, compatibility concerns with various web browsers or devices might surface, impacting the virtual terminal’s performance and potentially hindering seamless payment processing.

Regulatory Compliance and Legal Considerations

As a crypto investor, I understand the importance of safeguarding my financial information when making transactions online. Payment processors play a crucial role in this regard by adhering to strict regulatory guidelines. For instance, they must comply with standards like PCI DSS and GDPR to ensure secure handling of customer data. However, these regulations are subject to change or new mandates may emerge, necessitating updates to payment gateway systems and procedures. Keeping up with these modifications can be a challenging task for businesses, requiring them to remain agile and responsive in order to maintain compliance.

Virtual Terminal: Just like a payment gateway, the virtual terminal is obliged to observe regulatory guidelines on data security and privacy, with a focus on managing confidential payment details. Businesses providing services that use virtual terminals may additionally need to take into account industry-specific rules and legal stipulations concerning invoicing methods, consumer safeguards, and financial exchanges.

Customer Support and Troubleshooting

A Payment Gateway is essential as it ensures timely and efficient resolution of any technical hiccups or concerns regarding transaction processing. Delayed responses or subpar assistance can lead to dissatisfaction among merchants and consumers, potentially harming business performance and damaging customer relationships.

For businesses utilizing virtual terminals, encountering service interruptions or usability problems can disrupt normal operations. Swift assistance from customer support is essential to mitigate these disruptions. In the realm of service-based enterprises, specific concerns may arise, such as billing inquiries, transaction disputes, and industry-unique payment complications. To address these matters effectively, it’s crucial to have access to specialized support.

Picking the Right Version for Your Company

As a crypto investor, when it comes to choosing between a payment gateway and a virtual terminal, the decision depends on the specific needs and structure of your business. A payment gateway is an essential tool for facilitating online transactions, enabling seamless payments through websites or mobile applications. On the other hand, a virtual terminal is particularly useful for merchants handling mail or phone orders, allowing them to securely process payments over the phone or via email.

A payment gateway is an essential tool for e-commerce businesses, allowing customers to complete online transactions through multiple payment options such as credit cards, debit cards, and digital wallets. By smoothly integrating into websites and online platforms, it ensures a hassle-free experience for merchants while providing convenience and security for their customers during the checkout process.

As a researcher studying payment processing solutions, I’d describe a virtual terminal as follows: For merchants dealing with mail, phone, or even in-person transactions at events, a virtual terminal streamlines the payment process without requiring physical card readers. Instead, it enables merchants to accept payments from anywhere they have an internet connection.

Final Remarks

In simpler terms, understanding the differences between a payment gateway and a virtual terminal is essential for effectively managing your payment processing methods. Choose the appropriate option based on your business requirements to facilitate smoother transactions, boost security, and offer an effortless payment experience for your customers. Whether you select a payment gateway, a virtual terminal, or a combination of both, focus on optimizing efficiency and convenience to foster business expansion.

FAQs:

Which one is the cheapest virtual terminal?

As a crypto investor, I appreciate the flexibility that comes with using Square Virtual Terminal. Unlike some other services, there are no monthly fees or long-term commitments to worry about. Instead, you only pay a small processing fee each time you make a transaction. For remote transactions, it’s 3.5% plus fifteen cents, while for in-person payments, it’s 2.6% plus ten cents. This cost-effective and straightforward pricing model is a significant advantage for those of us who value convenience and control over our investments.

What is a PayPal Virtual Terminal?

PayPal’s Virtual Terminal is a user-friendly web application that enables merchants to process credit and debit card transactions without the need for physical swipe machines. This means merchants can take card payments over the phone, via fax, or through the mail.

What is the Sage Virtual Terminal?

As a researcher, I would describe Sage Virtual Terminal as follows: I utilize Sage Virtual Terminal, a secure online platform, for the purpose of examining, authorizing, or annulling ongoing transactions.

Which is the best free payment gateway?

As a payment gateway analyst, I would identify the following top free options for merchants: PaySimple, Dwolla, Spreedly, PayLane, Sila, CSG Forte, Payrexx, and HighRadius. Each of these providers offers robust payment processing solutions at no cost to you.

Which one is the best payment gateway for small businesses?

PayPal is widely used for transferring funds across borders. It supports more than 100 different currencies for transactions. With this platform, you can easily process both debit and credit card payments.

Read More

- WCT PREDICTION. WCT cryptocurrency

- The Bachelor’s Ben Higgins and Jessica Clarke Welcome Baby Girl with Heartfelt Instagram Post

- Royal Baby Alert: Princess Beatrice Welcomes Second Child!

- Guide: 18 PS5, PS4 Games You Should Buy in PS Store’s Extended Play Sale

- The Elder Scrolls IV: Oblivion Remastered – How to Complete Canvas the Castle Quest

- New Mickey 17 Trailer Highlights Robert Pattinson in the Sci-Fi “Masterpiece”

- AMD’s RDNA 4 GPUs Reinvigorate the Mid-Range Market

- Chrishell Stause’s Dig at Ex-Husband Justin Hartley Sparks Backlash

- SOL PREDICTION. SOL cryptocurrency

- Studio Ghibli Creates Live-Action Anime Adaptation For Theme Park’s Anniversary: Watch

2024-05-08 04:56