- The stablecoin market capitalization was trending upward once again

- One metric hinted at negative sentiment and selling pressure in the market

Stablecoins are an integral part of the crypto ecosystem. They’re typically tied to a fiat currency and exist on the blockchain with reserves held by external entities. Tether (USDT) is one of the most well-known stablecoins, backed by a vast reserve of USD. Other popular ones include USD Coin [USDC] and Dai [DAI], which are backed by USDC as well as other cryptos like Ethereum [ETH] and Bitcoin [BTC].

In simpler terms, stablecoins play a crucial role in the cryptocurrency world. They’re linked to real-world currencies, such as the US dollar, and are created on a blockchain with a corresponding reserve of that currency held by a trusted third party. An example of a widely used stablecoin is Tether, whose token is called USDT.

As a financial analyst, I would describe Tether as follows: I hold a substantial amount of U.S. Dollars in the form of cash or its equivalent in a reserve. Being a stablecoin categorized under the fiat-backed category, Tether maintains a strong link to the value of the U.S. dollar.

Among the numerous stablecoins available, USD Coin (USDC) and Dai (DAI) stand out as some of the most widely used. Notably, Dai is backed not only by USDC but also by other cryptocurrencies like Ethereum (ETH) and Bitcoin (BTC). As a result, DAI qualifies as a crypto-collateralized stablecoin.

Stablecoins provide a shield against cryptocurrency volatility, enabling holders to sell their digital assets and exchange them for stable coins. This vital feature ensures liquidity and keeps the value of stable tokens relatively steady even during significant market selling pressure.

One stablecoin to rule them all

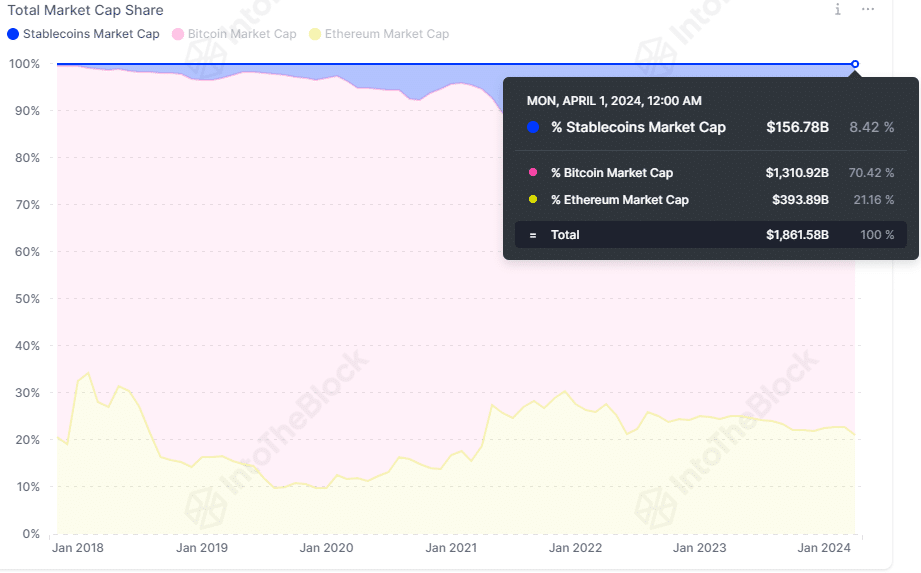

As a crypto investor, I’ve noticed that stablecoins hold a significant position in the cryptocurrency market. Specifically, they account for approximately 8.42%, which translates to a substantial $156 billion market capitalization.

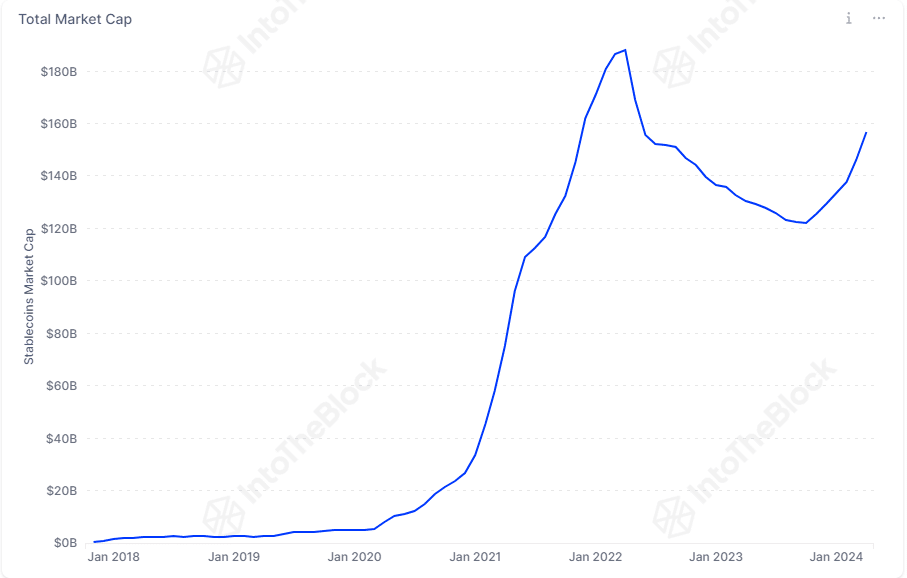

In April 2022, the stablecoins market reached its peak with a capitalization of $188 billion. However, during the bear market in 2022, this figure declined due to investors, disenchanted with crypto, returning to conventional assets and selling off their holdings.

Regulation related to cryptocurrencies significantly impacts the scenario. Paxos, the innovative firm behind the scene, generates Binance USD (BUSD) – a stablecoin that maintains parity with the US dollar in partnership with Binance.

In November 2023, the New York Department of Financial Services (NYDFS) issued a directive to Paxos, instructing them to halt the production of their stablecoin token. Subsequently, Binance declared their intention to phase out support for this particular stablecoin, causing BUSD’s market presence to wane.

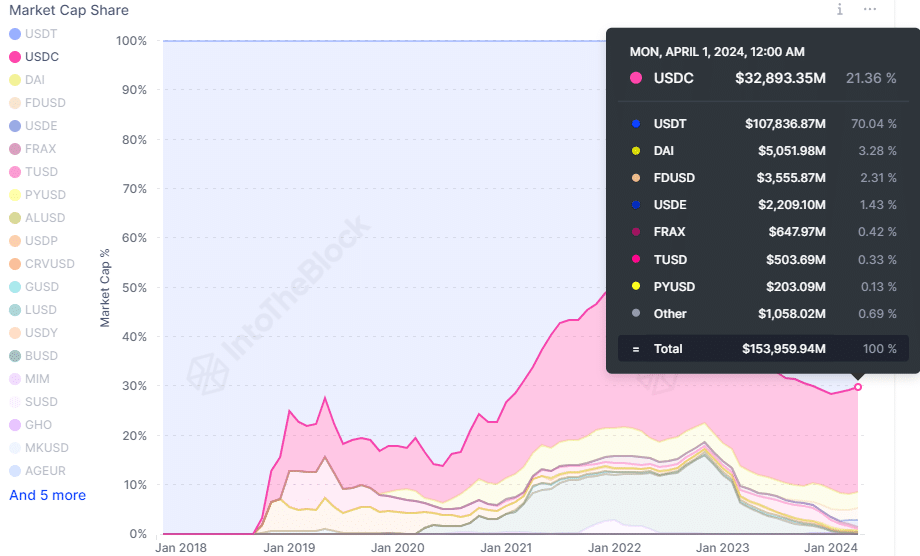

Among all stable tokens in the market, Tether holds the largest market share, accounting for approximately 70.04%. The second-largest contender is USDC, which represents around 21.36% of the total stable token market capitalization. Lastly, DAI comprises a relatively smaller portion with a market share of about 3.28%. This distribution underscores the market’s strong affinity for Tether.

With a longer presence in the market, they’ve weathered various rounds of fear, uncertainty, and doubt (FUD). Transparency regarding their asset reserves adds to customer trust.

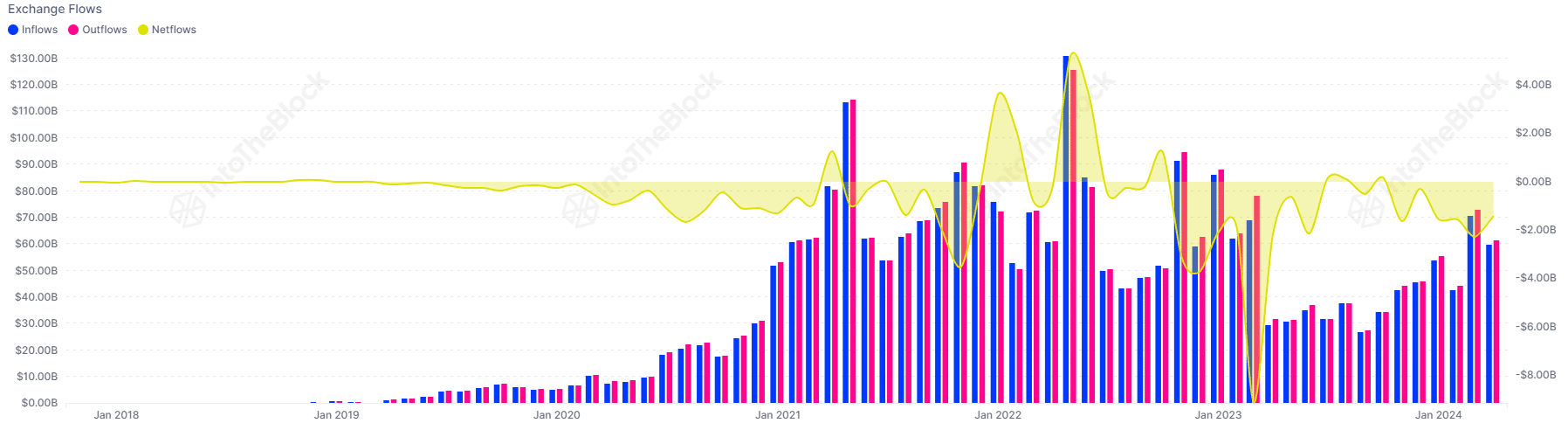

Gauging sentiment from stablecoin exchange netflow

Since October 2023, the total value of stablecoins in the market has risen significantly due to surging prices in Bitcoin and cryptocurrencies. This trend indicates greater purchasing power within the market and serves as a favorable signal.

Starting from November 2022, there has been a consistent outflow of stablecoins from cryptocurrency exchanges up until October 2023. This reverse flow suggests that there may have been heightened selling pressure over the past 18 months.

Read Bitcoin’s [BTC] Price Prediction 2024-25

As a researcher analyzing market trends, I observed a generally pessimistic sentiment reflected in this chart. Yet, there were two notable exceptions to this trend: substantial inflows of stablecoins occurred in January and May of 2022.

The inference of selling pressure leading to decreased trading activity and pessimistic sentiment based on netflow data is but one aspect of a intricate situation, and it does not encompass the entire story.

Read More

- PI PREDICTION. PI cryptocurrency

- Gold Rate Forecast

- WCT PREDICTION. WCT cryptocurrency

- LPT PREDICTION. LPT cryptocurrency

- Guide: 18 PS5, PS4 Games You Should Buy in PS Store’s Extended Play Sale

- Solo Leveling Arise Tawata Kanae Guide

- Despite Bitcoin’s $64K surprise, some major concerns persist

- Jack Dorsey’s Block to use 10% of Bitcoin profit to buy BTC every month

- Elden Ring Nightreign Recluse guide and abilities explained

- Shrek Fans Have Mixed Feelings About New Shrek 5 Character Designs (And There’s A Good Reason)

2024-04-29 09:11