MiCA Decoded is a twelve-article weekly dispatch for Bitcoin.com News, co-authored by LegalBison’s Co-Founding and Managing Directors: Aaron Glauberman, Viktor Juskin and Sabir Alijev. LegalBison advises crypto and FinTech companies on MiCA licensing, CASP and VASP applications, and regulatory structuring across Europe and beyond.

The Myth: You Can Get an Authorization in Just a Quarter

The crypto arena is not short on those who have memorized the regulation as if it were scripture. By 2026, most operators, legal teams, and advisers in the EU space have learned to stop quoting the 40-working-day figure as if it were a guarantee delivered by the postman of fate. That line, born of MiCA Article 63(9), is only a single rung on a much taller ladder, not the entire staircase.

The figure you actually hear in boardrooms and briefing decks is far more sober: three to six months, sometimes seven if the gods of bureaucracy are feeling particularly methodical. It factors in delays, regulator-to-applicant tango, and the friction of human hands on paper. In 2026, for seasoned lawyers poring over MiCA authorizations, that estimate often proves optimistic by a factor of two, or even three.

The realistic journey from submission to authorization for a well-prepared CASP filing with a major EU National Competent Authority (NCA) under current conditions stretches to 8-12 months, depending on the jurisdiction.

This article lays out, phase by phase, why the gap between dream and grit should be neither a surprise nor a novelty, but a structure to be understood and planned around.

Why the “1 to 3 Months” Estimate Falls Short

The one-to-three-month estimate is not born of ignorance. It is the impulse to strip the labyrinth down to a manageable diagram, a map that omits the mountains. The error lies in the proportions: the wrong variables in the wrong places, and the missing ones left in the drawer.

What the naïve model includes is the glimmer of a delay before assessment begins, a single regulator’s question round, and a dusty buffer for slowness. Each item is legitimate, but each is larger than common sense anticipates, and they march in sequence rather than side by side. There are other forces, namely the fit-and-proper scrutiny and hard calendar limits, that rarely appear in offhand planning conversations.

The result is a sketch that hints at the shape of the process but collapses its scale. What follows is the unembellished, uncompressed version.

Phase 1: The Completeness Gate

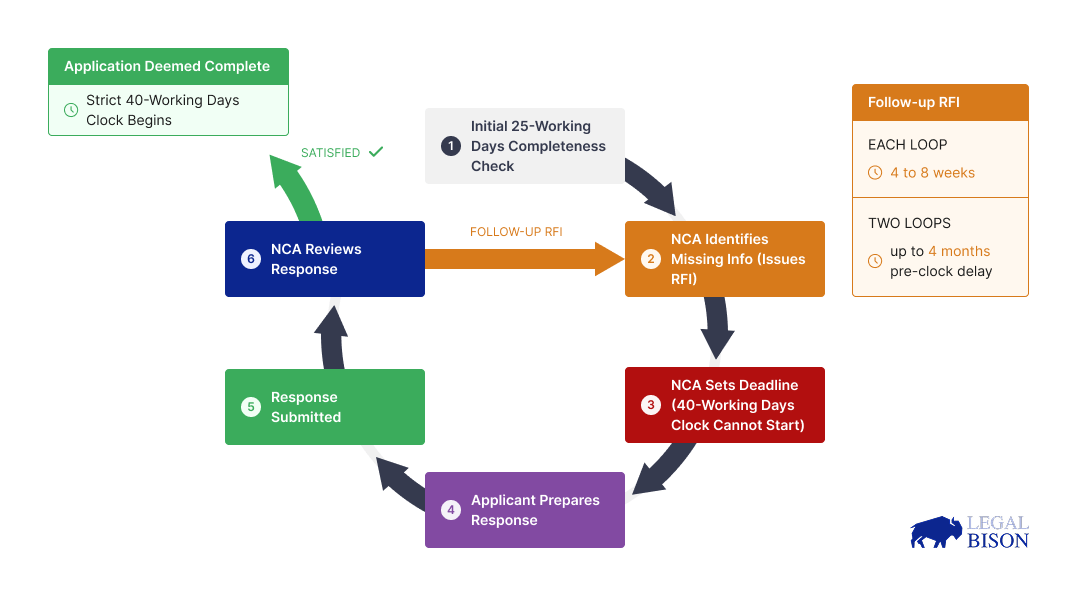

There is a number more critical than the start of the clock: 25 days. Under MiCA Article 63(2), an NCA enjoys up to 25 working days from the moment of receipt to judge whether the submission is complete, ensuring that every item required by Article 62(2) marches under the same banner.

The 40-day countdown does not begin at submission; it begins only when the NCA has formally deemed the submission complete and has notified the applicant under Article 63(4).

If the submission is found incomplete, the NCA issues a deadline to supply the missing information under Article 63(2). If that deadline is missed, the regulator may refuse to review the application, a polite way of saying you’ve failed the first gate with a flourish.

The process does not reset as if a restart button exists. Rather, missing details pursued through RFIs extend this initial phase significantly. An incomplete first submission can devour six to eight weeks before the formal assessment even begins.

Today, with many grandfathered firms pressing toward July 1, 2026, NCAs are operating at a gorge of capacity. The average completeness phase runs 45-60 days even for first-pass clearances.

The corrected understanding: The one-to-three-month estimate rarely treats submission as the actual starting point. In practice, a firm may spend the first two months simply proving its right to be considered before the 40-day clock under Article 63(9) has even begun.

Phase 2: RFI Cycles (The Pre-Clock Delay)

A structural feature of the MiCA process that industry players routinely underestimate is the Request for Information (RFI) cycle. Under MiCA Article 63(9) and 63(12), the formal 40-working-day assessment countdown cannot be legally paused for CASP applications. While the regulator can request more information during the assessment (no later than the 20th working day), the clock itself does not stop.

Because of this rigidity, regulators tend to use the pre-clock completeness phase to issue their expansive RFIs. They will not declare the submission complete until they are satisfied with the answers. The cumulative burden of producing substantive responses to multiple rounds of queries before the clock begins consumes significant time and legal resources. And this logic applies not only to CASPs: EMIs and credit institutions-the people who issue E-Money Tokens-face the same arithmetic of delay.

RFIs are a standard feature of how NCAs review complex CASP applications, covering governance, AML, market abuse monitoring, capital requirements, custody arrangements, and the fitness of management. The question, then, is not if an information request will arrive, but how many rounds of clarification precede the start of the 40-day clock.

The corrected understanding: Regulators cannot legally pause the 40-day clock, so they delay starting it. One to two RFI cycles are standard, and each cycle can take 4-8 weeks of pre-clock delay. A one-to-three-month estimate that accounts for some back-and-forth underestimates this variable.

Phase 3: MiCA Fit and Proper Assessment Is Not a Checkbox

Authorization under MiCA is not merely a test of systems, policies, and capital. It is a test of the people who will run the enterprise. Under Article 68(1), members of the management body must show good repute and the knowledge, skills, and experience to perform their duties both individually and collectively.

Under Article 68(2), shareholders with qualifying holdings face a separate good-repute assessment. Article 63(10) makes clear that the NCA must refuse authorization if the management body poses a threat to prudent and effective management, or if its members fail to meet the criteria of Article 68(1).

This is not a mere formality; it is a substantive test, and in 2026 it has grown more demanding than many planning conversations anticipate.

NCAs in several major jurisdictions-France and Ireland among them-now routinely schedule live interviews with management figures as part of the fit-and-proper evaluation. These interviews probe regulatory awareness, governance judgment, and the precise experience that justifies licensing a modern financial creature into the wild.

The scheduling of these interviews is where fear and folly meet. Regulator availability, holidays, and heavy caseloads mean a company whose submission is otherwise complete may wait four to six weeks simply for an interview date.

The 40-day clock continues to run during this period, but because authorization cannot be granted until the fit-and-proper assessment is resolved, the practical effect is the same as a suspension.

The corrected understanding: The fit-and-proper assessment under Article 68 is a mandatory, substantial requirement, not a mere procedural tick. While MiCA requires the place of effective management to be in the EU and at least one director to be an EU resident, regulators will test the substantive competence of the whole management body. When NCAs insist on live interviews to verify this collective fitness, the scheduling lag becomes four to six weeks of lead time beyond the applicant’s control.

Phase 4: Calendar Events Slowing Down the Process

Above the formal ritual lies a calendar, indifferent and unyielding. NCAs are public bodies. They honor national holidays, fleets of leave, and the slow rhythm of seasonal tides. Some periods of the year simply move slower, regardless of quality or responsiveness.

This is not mischief; it is institutional habit. The seasoned practitioner builds this friction into every timetable from the start.

| Calendar Factor | Typical Timeline Impact |

| August slowdown | 3 to 4 weeks; key personnel and case officers on leave across most EU jurisdictions |

| December-January break | 3 to 4 weeks; reduced NCA capacity through the holiday period |

| Public holiday clusters | 1 to 2 weeks per cluster; particularly relevant in jurisdictions with extended national holiday periods |

| NCA caseload peaks | Variable; the 2026 grandfathering deadline under Article 143(3) has created a structural backlog across multiple NCAs |

| Local legislative delays | Variable; some jurisdictions have experienced processing delays pending full domestic implementation of MiCA provisions |

| Understaffing | NCAs are simply limited by their manpower. We all remember the AMF in France taking more than 2 years to deliver DASP licenses (before MiCA) as staff scattered toward Binance, leaving regulators with thin teams. |

The 2026 context adds a multiplier to every row. Under Article 143(3) of MiCA, crypto-asset service providers that offered services lawfully before 30 December 2024 may continue until 1 July 2026, or until authorization is granted or refused under Article 63, whichever comes first. The volume of applications arriving simultaneously at NCAs already near capacity has produced a backlog that affects processing times across the board.

The corrected understanding: Calendar friction is not a soft risk; it is a hard, stubborn fact. In practice it adds three to six weeks overall to almost every authorization and can stretch much longer if timing is unlucky.

The Reality of the Timeline: Why Good Applications Still Stall

A technically flawless submission is not immune to the drift of calendar and temperament. Founders tend to structure their launches around statutory times, underestimating the human and administrative variables that govern the cadence of a National Competent Authority.

To craft a credible timeline, prudent planners build in the following truths:

- The “Completeness” Gate Delays the Clock: Under Article 63(9), the formal 40-working-day assessment begins only after the NCA officially deems the application complete. If the regulator asks for additional documentation during the initial 25-working-day review (for instance, more source-of-wealth data for a beneficial owner), the clock pauses until the information is provided.

- Calendar Drag and Human Factors: NCAs are run by people with regular hours, holidays, and vacation. Submitting in late November or just before holidays invites weeks of “calendar drag.”

- The Fit and Proper Scheduling Lag: As noted, the management-body assessment under Article 68 is substantive. When live interviews are required, aligning the executive team’s schedule with the regulator’s availability can easily add four to six weeks of lead time, entirely beyond the provider’s control.

The takeaway: A four-to-five-month expectation that becomes a six-month reality is not a regulatory apocalypse, but a business truth. When you align operational readiness, capital deployment, and market timing around a MiCA authorization, it is not the speed that matters but the predictability of the schedule.

The Complete Picture

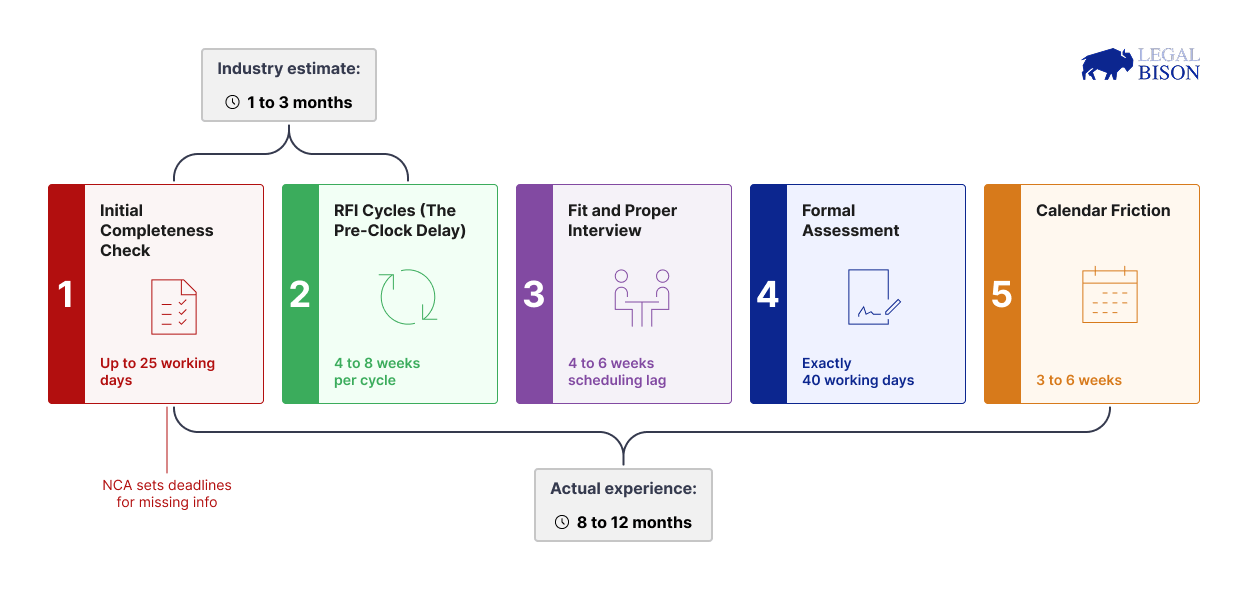

Here is the full MiCA CASP authorization timeline, mapped phase by phase:

Phase 0 – Pre-Requisite Corporate Structure: A MiCA CASP authorization is granted to a legal entity (or equivalent). The entity requires a credit institution account to hold share capital and must be structured to satisfy strict operational and substance requirements, namely, the place of effective management must be in the EU, and at least one director must be an EU resident. The entity must be fully compliant with MiCA and DORA regulations governing resilience and auditing of its ICT infrastructure. We call it “Phase 0” as the structural foundation, though it can run in parallel with other stages to some extent.

Phase 1 – Initial Completeness Check: Up to 25 working days. The NCA reviews the submission to determine if all required information is present. If anything is missing, they set a deadline for the applicant to provide it.

Phase 2 – RFI Cycles (The Pre-Clock Delay): One to two cycles are standard. Each cycle takes 4 to 8 weeks. Because regulators cannot pause the formal assessment clock, they use this pre-clock phase to issue RFIs and resolve all missing details.

Phase 3 – Fit and Proper Interviews: Scheduling lead time of 4 to 6 weeks in jurisdictions that require live interviews. This, too, is typically settled before the NCA stamps the submission as complete.

Phase 4 – Formal Assessment: Exactly 40 working days. This countdown begins only after Phases 1 through 3 are resolved and does not pause. If final clarifications arise, they must be issued by the 20th working day without stopping the clock.

Phase 5 – Calendar Friction: 3 to 6 weeks in aggregate. Submission timing, holidays, staff leave, and backlogs across jurisdictions compound the effect.

Realistic total: 8 to 12 months from submission to authorization.

The one-to-three-month instinct is not wrong in its instincts; it identifies the landscape. It simply misses the true scale of the terrain. The ESMA CASP register shows authorizations taking this long not from inefficiency or malice, but because a rigorous assessment of an entity’s fitness to operate in regulated markets is genuinely intricate, and complexity demands time.

Understanding this, with enough precision to model each phase, is what saves a timeline from being a rumor and turns it into a navigable map.

Key Takeaways:

1. The industry estimate of 1 to 3 months remains dangerously optimistic. It grasps the right instincts but compresses the scale of each variable. A realistic figure for a well-prepared application under current conditions is 8 to 12 months.

2. Submission is not the start line. The 40-working-day assessment only begins after the NCA declares an application complete. The completeness check is a separate phase with up to 25 working days to identify missing information; failure to provide it can bar the review altogether.

3. RFIs stall the timeline, but they do not pause the 40-day clock. Under MiCA, the countdown does not stop for CASPs. Regulators may request information up to the 20th working day, but the clock keeps ticking. Therefore, factor in at least one multi-week RFI cycle in any realistic plan.

4. The fit and proper assessment covers the management body and qualifying shareholders. Article 68(1) requires governance virtue and competence; Article 68(2) looks to shareholders’ good repute. Live interviews are increasingly standard; plan for a 4-6 week scheduling lag.

5. August and December are structural delays, not soft risks. An overlap with these windows guarantees a default delay of 3-4 weeks, regardless of quality.

6. The grandfathering deadline is a hard cliff, not a rolling extension. Firms that operated pre-December 2024 may continue until 1 July 2026 or until authorization is granted or refused, whichever comes first. This is a legal cliff, not a margin of error. If a state trims the transitional period, the cliff arrives sooner still.

7. Pre-application preparation is where the battle is actually won (or lost). Retrofitting compliance after filing is often too late. Building structural independence, conducting collective suitability assessments, and aligning with MiCA’s stringent data and governance standards requires architecture before the regulator, not repair after the fact. Partnering with seasoned counsel who understand the regulatory machinery is not a luxury; it is a necessity.

This article was produced in partnership with LegalBison. The content is for informational purposes only and does not constitute legal advice.

Read More

- The Super Mario Galaxy Movie: 50 Easter Eggs, References & Major Cameos Explained

- Surprise Isekai Anime Confirms Season 2 With New Crunchyroll Streaming Release

- 10 Best Free Games on Steam in 2026, Ranked

- ‘Project Hail Mary’: The Biggest Differences From the Book, Explained

- Preview: Sword Art Online Returns to PS5 as a Darker Open World Action RPG This Summer

- Starfield (PS5) Review – A Successful Cross-Console Voyage

- Sydney Sweeney’s The Housemaid 2 Sets Streaming Release Date

- Why is Tech Jacket gender-swapped in Invincible season 4 and who voices her?

- Skate 4 – Manny Go Round Goals Guide | All of the Above Sequence

- Overwatch 2 G.I. Joe Crossover Launches July 1: Join the Battle Between Heroes and Villains

2026-04-12 09:57