Oh, the meticulous Japanese! They’ve crafted a stablecoin framework so rigid, it makes a samurai’s code of honor look like a suggestion box at a tea ceremony.

Japan’s Stablecoin Farce

Behold, JPYC Co., the first to unleash a yen-pegged stablecoin upon the world in October 2025! A decade of financial navel-gazing by Tokyo’s bureaucrats has finally borne fruit-or should we say, a meticulously pruned bonsai tree of regulation?

The Financial Services Agency (FSA), those guardians of fiscal prudence, spent years weaving a web so intricate, even a Terra/Luna collapse would bounce off it like a rubber ball. Their Payment Services Act amendments are a masterpiece of red tape, ensuring only the most obedient entities may issue these “digital-money type stablecoins.”

Who Dares Issue? A Comedy of Eligibility

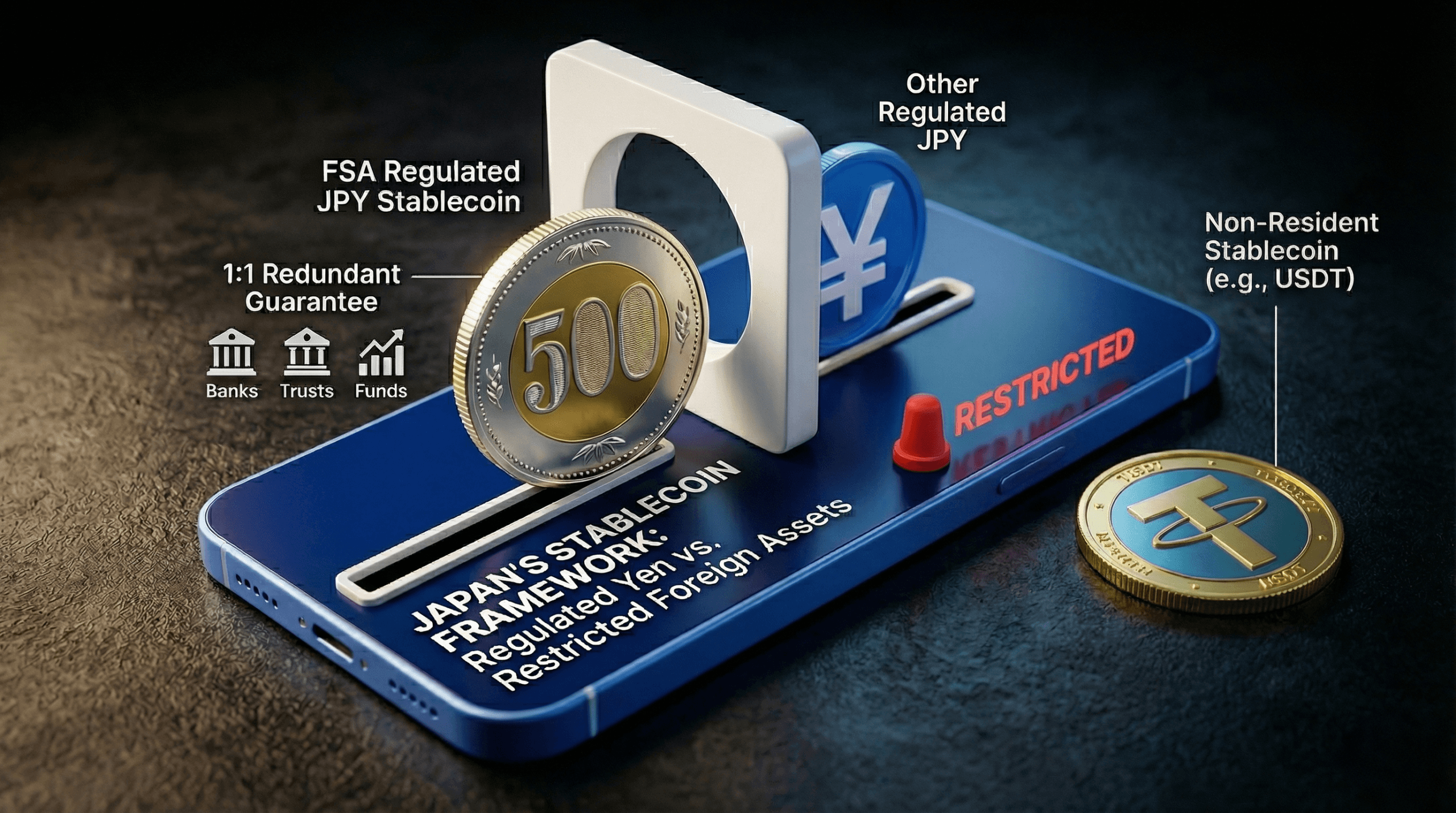

Only banks, fund transfer service providers, and trust companies need apply-a trio of financial gatekeepers. Banks, those pillars of tradition, issue stablecoins as deposits, nestled safely under Japan’s deposit insurance blanket. Fund transfer providers, ever the pragmatists, back their tokens with money deposits, bank guarantees, or the sacred Japanese government bonds. Trust companies, the custodians of virtue, hold all assets as bank deposits, with a post-2025 twist: up to 50% in low-risk short-term instruments, because why not add a dash of spice to the stew?

JPYC, the plucky pioneer, secured its fund transfer license in August 2025. Its token, running on Avalanche, Ethereum, and Polygon, promises a 1:1 yen reserve and zero transaction fees. Revenue? A modest sip from the JGB interest pool. Their ambition? A staggering 60 trillion yen in circulation within five years. Cross-border payments, remittances, and Web3 settlements-nothing short of financial world domination, one yen at a time.

The FSA, haunted by the ghost of Terra/Luna, has enshrined redemption at par as the holy grail. Every issuer must swear fealty to this guarantee, or face exile to the crypto-asset wilderness. A run on the system? Unthinkable! Japan’s regulators have built a fortress, and woe betide the stablecoin that dares breach its walls.

Dollar Stablecoins: The Uninvited Guests

Alas, poor USDT and USDC! Dominating 97 to 99% of the global stablecoin market, yet in Japan, they are but shadows. Foreign issuers like Tether and Circle must navigate a compliance labyrinth that would make Theseus blush. Japanese exchanges, ever cautious, have largely shunned these dollar-denominated interlopers.

USDT remains a rare sight on Japanese platforms, while USDC enjoys a limited sojourn via SBI VC Trade, thanks to Circle’s alliance with SBI Holdings. But access is capped, a mere trickle for retail users. Japan’s preference for yen-denominated assets is not just regulatory-it’s cultural. A cash-heavy economy, regional remittances, and trade in yen have rendered dollar liquidity tools as useful as a fan in a typhoon.

Banks: The New Stablecoin Aristocracy

Japan’s banking titans-MUFG, SMBC, and Mizuho-are not ones to miss the stablecoin bandwagon. Through the Progmat platform, they develop trust-based yen stablecoins, while SBI Holdings plans its own launch in Q2 2026. The JPY stablecoin market cap, a modest $36.6 million as of early 2026, may seem small, but it grows in the fertile soil of institutional and cross-border payments.

Middlemen: The Unsung Compliance Heroes

Intermediaries, those unsung heroes of the financial world, face their own trials. Registered as Electronic Payment Instrument Exchange Service Providers, they must keep 95% of customer crypto-assets in cold storage, segregate funds in trust structures, and comply with FATF Travel Rule requirements. Liability-sharing agreements with issuers? Check. Losses from bankruptcy, hacks, or technical failures? Covered. It’s a regulatory ballet, and every step must be perfect.

The 2025 PSA Amendment Act, enacted in June 2025, offers a glimmer of mercy: a lighter category for pure brokers, relaxed reserve rules for trust-type issuers, and more flexibility for cross-border handling. FSA consultations in January 2026 pondered eligible bond types, while the agency mulls shifting certain crypto-assets from PSA oversight to the Financial Instruments and Exchange Act. A regulatory shuffle, but stablecoins remain firmly in the FSA’s grasp.

A History of Caution: From Mt Gox to Stablecoin Supremacy

Japan’s regulatory journey began with the Mt Gox debacle in 2014, a catastrophe that spurred the first PSA crypto amendments by 2016. Exchange registration, user asset segregation, and AML compliance became the law of the land. Stablecoins, then mere infants, received scant attention. Early experiments like JPYC’s predecessor and Hokkoku Bank’s Tochika token were but precursors to the current regime.

Japan’s system is a study in tradeoffs. It moves with the grace of a tortoise, favors domestic issuers like a protective parent, and sidelines global stablecoins with bureaucratic finesse. Yet, it delivers: every yen-pegged token carries a redemption guarantee, a licensed issuer, a segregated reserve, and FSA oversight. A Tokyo retail user, a megabank treasury desk, or a foreign exchange listing USDC-each sees a different reflection in this regulatory mirror.

The Future: A Slow Waltz of Bank Launches and Interoperability

More bank launches are on the horizon in 2026. JPYC, ever ambitious, expands interoperability through partnerships with Circle and TIS for enterprise payments. The framework that once stifled stablecoin activity now nurtures regulated domestic issuances. Whether this pace satisfies the market is one question; whether the system works as designed is another.

FAQ 🔎

- What stablecoins are legal in Japan? Only yen-pegged digital-money type stablecoins issued by FSA-licensed banks, fund transfer service providers, or trust companies may grace Japanese wallets.

- Is USDC or USDT available in Japan? USDT remains a rare sight, while USDC enjoys limited access via SBI VC Trade under Circle’s partnership.

- What is JPYC? JPYC, the first fully regulated yen-pegged stablecoin, debuted in October 2025, a child of Japan’s revised Payment Services Act.

- Why does Japan restrict foreign stablecoins? The FSA demands that all stablecoin issuers meet the same stringent standards as domestic entities-a bar too high for most foreign issuers to clear.

Read More

- Best Controller Settings for ARC Raiders

- Review: Final Fantasy Tactics: The Ivalice Chronicles (PS5) – Still the Benchmark for Turn-Based Tactics

- Nippon Sangoku Is The Best New Post-Apocalyptic Anime of Spring 2026

- Mark Zuckerberg & Wife Priscilla Chan Make Surprise Debut at Met Gala

- 10 Greatest Manga Endings of All Time

- The Witcher 3 Officially Reveals Stunning New Ciri Figure Coming 2026

- The WONDERfools ending explained: What happened to the Child of Eternity?

- 7 Great Marvel Villains Who Are Currently Dead

- FRONT MISSION 3: Remake coming to PS5, Xbox Series, PS4, Xbox One, and PC on January 30, 2026

- Elon Musk’s Mom Maye Musk Shares Her Parenting Philosophy

2026-04-03 15:28