what the blockchain actually does and what significance it has within the broader crypto ecosystem?

Five months after its November 2025 mainnet launch, Monad confronts a harsher reality: impressive technology paired with minimal revenue, a token down roughly 40% from its all-time high, and tokenomics that heavily favor insiders. One might call it a “ghost chain” if one were being cruel-and who isn’t, in the world of blockchain?

While the chain demonstrates genuine engineering ambition, questions remain about whether hype can sustain it amid thin on-chain economics and looming dilution. After all, even the most elegant machine cannot outpace the laws of arithmetic.

A brief suspension becomes narrative victory

The X suspension triggered an immediate 9% dip in the blockchain’s native MON token, reflecting the account’s central role in community coordination and announcements. Co-founder Keone Hon publicly stated there was “no abnormal activity” on their end and attributed the flag to an automated system. The account returned swiftly, likely after manual review. One suspects the manual reviewer was a weary intern clutching a coffee and a dictionary.

For a project built on speed and performance claims, turning a routine platform enforcement into a celebrated “win” highlights a reliance on optics. Crypto observers noted the irony: a chain promising 10,000+ TPS celebrated basic account restoration while daily fees struggled to break $4,000. The episode underscores how early-stage L1s often prioritize social momentum over metrics in volatile markets. A performance so dazzling it could make a pigeon envious.

Massive capital in vs. razor-thin revenue out

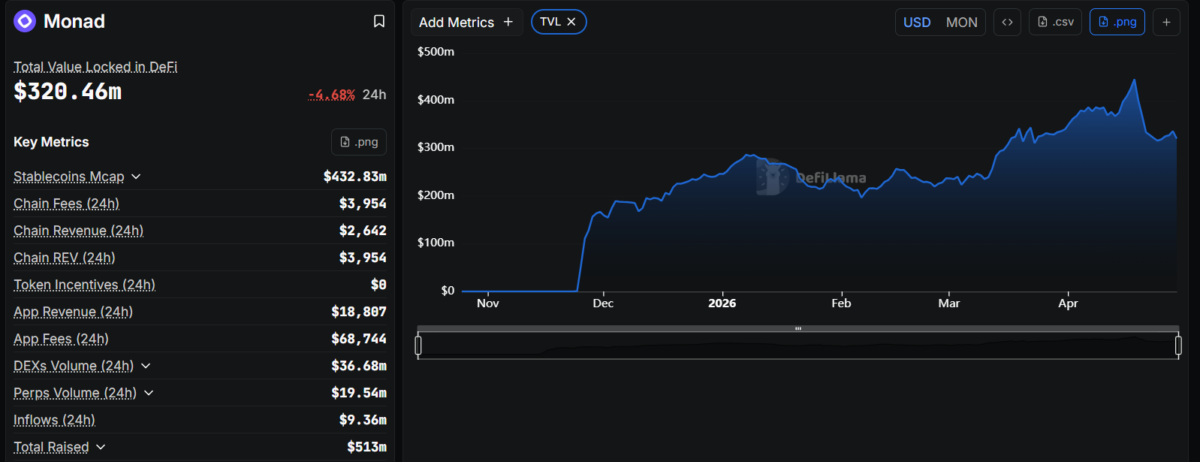

As of late April 2026 shows Monad’s DeFi total value locked (TVL) at approximately $320 million, with bridged assets pushing totals higher (stablecoin market cap around $433 million). Despite attracting such an attractive TVL amount within five months of mainnet, a closer look at Monad’s on-chain metrics reveals a fragile foundation. One might liken it to a house of cards built on the hope that no one will sneeze.

According to DeFiLlama, a substantial portion of this liquidity-roughly $642 million in bridged assets-consists of capital teleported from Ethereum, Solana, and other chains, dominated by stablecoins such as USDC. Much of the TVL sits in lending protocols like Morpho Blue ($143 million) and yield aggregators, where users park assets for passive returns rather than actively using the chain’s vaunted parallel execution engine. It’s a bit like inviting guests to a banquet and then serving them stale crumpets.

This pattern suggests mercenary capital chasing temporary yields rather than genuine ecosystem building, raising concerns that the headline TVL figure overstates organic adoption. The numbers may dance, but the orchestra is playing a different tune.

Moreover, the disconnect between capital raised and actual economic activity is particularly stark. Monad has secured over $513 million in total funding, yet its 24-hour chain fees currently hover between $3,954 and $4,188, generating just $2,642-$2,753 in daily revenue for the network. This results in one of the lowest fee-to-TVL ratios among comparable Layer 1s. One wonders if the project’s engineers have ever heard of compound interest.

Monad’s annualized revenue remains in the low six figures-a negligible return on the project’s massive valuation. Critics argue this reflects a high-performance “ghost chain”: technically capable of 10,000+ TPS but failing to drive sustained, fee-generating usage beyond low-gas speculative flows. A technological marvel with the appetite of a sparrow.

Its onchain behavior further underscores the gap between hype and reality. The daily DEX volume on the chain sits at approximately $36.7 million and perpetuals at $19.5 million, but much of this appears to be arbitrage, wash trading, or incentive-driven activity rather than organic user demand. It’s a carnival of numbers, but the ticket booth is closed.

With network utilization reportedly below 1% of theoretical capacity and no breakout consumer applications or gaming ecosystems, Monad’s activity remains concentrated in basic DeFi primitives. One might say it’s a blockchain that prefers to sit in the corner and sip tea while the rest of the industry dances.

As incentives taper and major token unlocks approach in late 2026, the project faces a critical test: can it convert bridged liquidity and speculative interest into durable economic activity, or will it join previous high-hype L1s that faded once the initial capital inflows subsided? Only time will tell, though time is a fickle companion in the world of crypto.

Token performance: 40% below ATH reflects market caution

At the time of publishing, MON was trading around $0.029, down approximately 40% from its all-time high of ~$0.0488 reached shortly after mainnet in late November 2025. The token’s circulating market cap sits near $348 million, with fully diluted valuation (FDV) exceeding $2.96 billion. A performance so lackluster it could make a sloth blush.

Token’s all time chart shows a downward trend since launch, reflecting post-hype gravity. The project’s large unlocks and broader skepticism toward high-FDV L1s have weighed on sentiment. It’s a rollercoaster ride with the brakes on and the track in reverse.

Even Arthur Hayes, one of the most prominent voices in the crypto industry, flagged it as a high-risk VC play susceptible to dilution. Retail participants who entered on scalability promises now hold positions well underwater. One might say they’ve been handed a life preserver made of wet newspaper.

Monad tokenomics: Insider-heavy structure fuels dilution fears

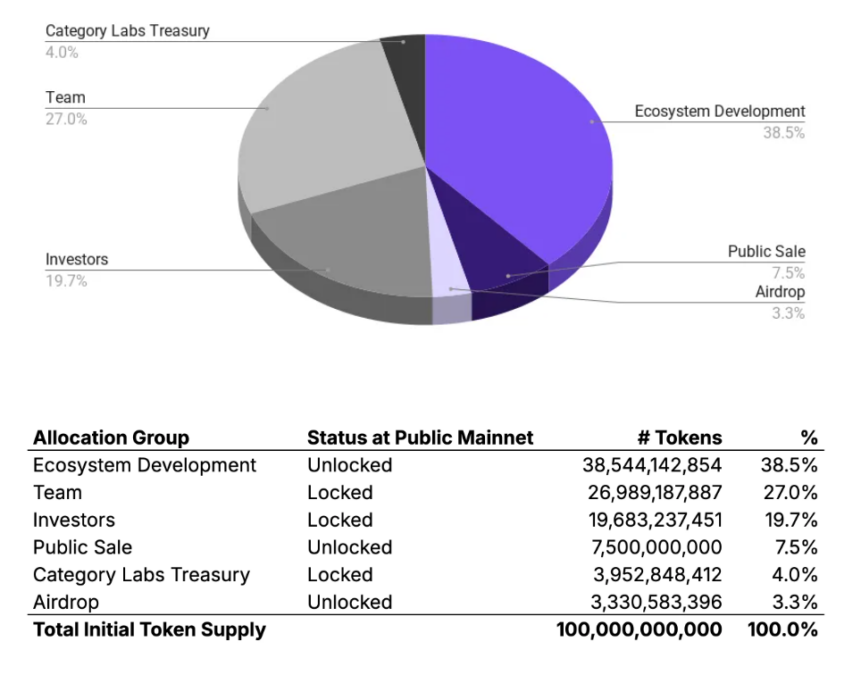

Tokenomics are the most important aspect for a blockchain as it is used to calculate both the project’s current and future state of economy. Monad has a total supply of 100 billion tokens, out of which, roughly 11.83 billion tokens are in circulation. A gilded cage for investors, perhaps, with the key held by the very birds inside.

Monad’s tokenomics feature a balanced but heavily foundation-weighted distribution designed to support long-term ecosystem growth while aligning incentives through vesting. Ecosystem Development receives the largest share at 38.5%, fully unlocked at TGE and stewarded by the Monad Foundation for grants, incentives, validator delegations, and partnerships over many years. A feast for the foundation, a crumb for the rest.

The Team allocation of 27% has a 1-year cliff followed by 48-month linear vesting, as does the Investors portion at 19.7%. Smaller slices include Public Sale at 7.5%, Airdrop at 3.3%, and Treasury/Category Labs at approximately 4%. A pie so delicately sliced it could make a pâtissier weep.

At mainnet launch, roughly 49.4% of the supply was unlocked (primarily from ecosystem, public sale, and airdrop), with the remaining ~50.6% locked and vesting gradually through 2029 to limit immediate selling pressure. A game of patience for the patient, and a gamble for the rest.

At launch, only ~10.8-11.8% entered broad circulation. The large unlocked ecosystem bucket gives the foundation significant flexibility for grants and incentives, but also centralized influence. A velvet glove over an iron fist, perhaps, or a silk scarf wrapped around a noose.

Community criticism centers on the structure: high FDV, low initial float, and perceived favoritism toward VCs and KOLs over retail (the airdrop was notably small). No widespread confirmed large insider exits have surfaced due to vesting, but the design inherently sets up future sell pressure. A slow burn, with the match lit by the very architects.

Various analysts have described it as a classic “VC coin” where early backers are positioned to realize gains while later holders absorb dilution risks. A game of musical chairs where the chairs are made of sand.

Technical promise vs. economic and adoption hurdles

Monad’s core innovations-parallel optimistic execution, MonadBFT consensus, asynchronous pipelining, and MonadDB-earn technical respect. Full EVM compatibility enables seamless dApp migration, and the chain has onboarded DeFi primitives, DEXs, and partnerships. A symphony of code, if one ignores the audience snoring in the front row.

Its TVL growth to over $300 million in months demonstrates capital attraction. Yet the path forward is narrow. Sustained organic usage, not incentive-driven TVL, will determine success. A bridge built on hope and a handshake.

Competition is fierce, and November 2026 unlocks loom as a key test. If revenue remains minimal and adoption fails to accelerate, the project risks joining prior high-hype L1s that faded after initial excitement. A phoenix with a short fuse.

The recent X suspension episode, while trivial in isolation, encapsulates Monad’s current phase: adept at narrative spin but challenged by translating technical edge into durable economic value. A magician who forgot to practice the trick.

Final words

Despite its genuinely impressive technical innovations and parallel execution architecture, Monad currently feels like yet another classic VC-driven Layer 1 project designed to extract capital from the broader crypto ecosystem-only with an extra step. A confection wrapped in a bow of ambition.

The project masterfully layers heavy marketing, social media drama, and narrative spin on top of the familiar playbook of massive funding, high FDV, low-float tokenomics, and mercenary liquidity. A stage play where the actors forget their lines but keep bowing anyway.

While the engineering deserves respect, the thin on-chain revenue, reliance on bridged speculative capital, looming unlocks, and celebration of minor incidents like an X account restoration reveal a project still struggling to move beyond hype into sustainable value creation. A mirage with a ticket price.

Until Monad can translate its performance promises into real economic activity and organic usage, it risks remaining just a more sophisticated version of the same old story. A tale as old as time, but with more zeroes and fewer dragons.

Read More

- Best Controller Settings for ARC Raiders

- Review: Final Fantasy Tactics: The Ivalice Chronicles (PS5) – Still the Benchmark for Turn-Based Tactics

- Mark Zuckerberg & Wife Priscilla Chan Make Surprise Debut at Met Gala

- The Boys Season 5 Officially Ends An Era For Jensen Ackles’ Soldier Boy

- Nippon Sangoku Is The Best New Post-Apocalyptic Anime of Spring 2026

- Elon Musk’s Mom Maye Musk Shares Her Parenting Philosophy

- 10 Greatest Manga Endings of All Time

- The Witcher 3 Officially Reveals Stunning New Ciri Figure Coming 2026

- The WONDERfools ending explained: What happened to the Child of Eternity?

- 7 Great Marvel Villains Who Are Currently Dead

2026-04-29 14:37